Viva Leisure

Mitch Ryan, Senior Analyst

You should read the Fund’s Target Market Determination (TMD) and the Fund’s Product Disclosure Statement (PDS) to ensure the key attributes of the Fund as described in the TMD and PDS aligns with your objectives, financial situation and needs. These documents are available on the Apply Now page on this website.

Working hard for gains

We have chosen to highlight Viva Leisure as our stock in focus this quarter, a stock we hold in the NovaPort Microcap Fund. We initiated a position in Viva Leisure at its IPO in June this year.

Viva Leisure is a rapidly expanding health club operator focussed on regional cities and towns such as Canberra, Ipswich and Wollongong. We initiated a position in Viva Leisure for its strong multi-tiered growth trajectory being implemented by a highly aligned management team. Following, we examine Viva’s operating platform and how it positions the company for growth.

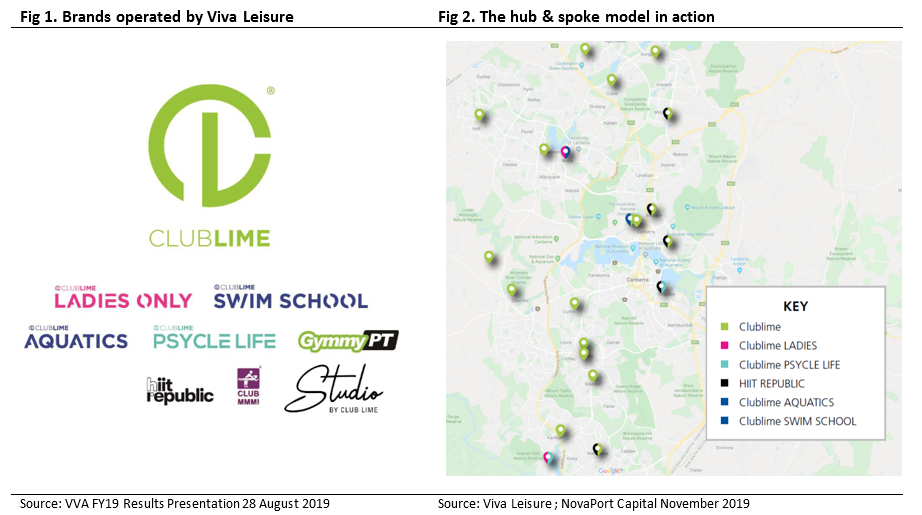

First, Viva operates a flexible hub and spoke model that it adapts to match the demographics and demand of each area that it operates in. This allows it to setup one larger big-box facility and several smaller boutique ancillary facilities over time as membership within a region grows. The satellite gyms may be either a standard, express or boutique club. The model allows Viva to rapidly grow its number of locations and membership base. Whereas its competitors to date have traditionally concentrated in one segment (i.e. big box, standard, express or boutique health clubs).

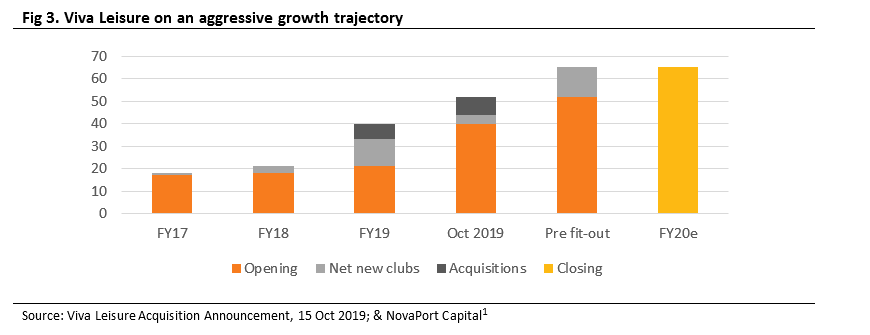

Viva Leisure’s operating structure enables the company to implement its rapid growth ambitions via a mix of acquisition and organic. The company has been on a growth offensive of late that has seen it grow club numbers from 21 at the end of FY18 to now being at 52 operating locations with a further 13 locations at different stages of fit-out. Once it acquires a club in an area Viva is able to use this as a beach head to then add satellite studios which delivers two outcomes:

- It increases the membership density of an area; and

- Increases the value existing members perceive they are receiving from their membership.

The third area of attraction is that the company is improving the average membership rate that people are prepared to pay by adding access to the specialised boutique studio’s – Psycle Life and HIIT Republic. The company has recently added the HIIT republic brand which offers a High Intensity Interval Training (H.I.I.T) similar to F45 Training. Members pay a higher rate than the standard Club Lime fee to gain access to the HIIT Republic offering. A multi-club membership for just Club Lime facilities is $21.50/week compared to $39.90/week for multi club HIIT Republic and Club Lime membership. The diversity of training options increases members affiliation with the Viva offering, helps with retention and adds new members.

As pointed out in this quarters Market Insight, the market can become too enamoured with the growth narrative and lose track of the underlying earnings growth. As such, we’re attracted to the fact that our forecasts for Viva see EPS to grow at a CAGR of ~30% from FY19 to FY22. Beyond which we forecast a slowing to a mid-teen EPS CAGR between FY22-FY251.

Risks to consider

We have seen gym offerings stumble when in the listed arena before (Ardent Leisure) and are not naïve to the risks associated with an investment in the sector. We see a multitude of components driving the decision-making process for gym membership, including:

- convenience of location;

- pricing;

- quality of facilities; and

- fitness trends.

As a corollary we also see all of these as engendering the key risks to our investment in Viva Leisure. We believe that Viva’s business model allows it to address most of these concerns. Specifically, it’s Hub and Spoke model allows for a high density of locations within a geographic region, that offer a suite of training options which can be tailored to the prevailing trends of the day. To date the company has shown it is able to price appropriately for its target markets and maintain high quality facilities.

Another area of focus is the way in which Viva is able to differentiate its offering to that of existing chains (e.g. Fitness First and Virgin Active). For us, one of the key differentiators is the technology sitting behind the physical locations. Viva’s technology platform delivers the following benefits:

- Frictionless

sign-on

- Members can join in under 3 minutes with potentially no staff contact.

- Giving control to

members

- Members are able to enter facilities using just the RFID of their mobile device

- Members can monitor their attendance and process membership pauses via the member portal

- Monitoring at

risk members

- Viva is able to utilise significant live data metrics to identify the overall cancellation risk of a member. They utilise this to contact these members to offer solutions that improve retention.

Summary

Viva’s share price has appreciated significantly since we initially established a position at its IPO, that said we continue to hold a constructive view on Viva’s growth pipeline. We remain attracted to the stock for its increasing club locations, growing membership rates at these clubs and increasing average monthly membership rate all while increasing member engagement.

1 Information is predictive in nature and may differ materially from actual figures. The information is based on NovaPort Capital’s reasonable assumptions and is presented here solely to illustrate NovaPort Capital’s research capability.

The information in this article is current as at the date of publication and is provided by NovaPort Capital Pty Ltd ABN 88 140 833 656 AFSL 385329 (NovaPort), the investment manager of the NovaPort Smaller Companies Fund ARSN 094 601 475 and NovaPort Microcap Fund ARSN 113 199 698 (the Funds).

It is intended to be general information only and not financial product advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider the applicable disclosure document or product disclosure statement (PDS) and any additional information booklet for the relevant Fund before deciding whether to acquire or continue to hold an interest in the relevant Fund. The relevant PDS can be obtained from your financial adviser, Fidante Partners’ Investor Services team on 13 51 53 or website www.fidante.com.au. Please also refer to the Financial Services Guide on the Fidante Partners website. Past performance is not a reliable indicator of future performance. Neither your investment nor any particular rate of return is guaranteed.

Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante Partners), is the responsible entity of the Funds. Other than information which is identified as sourced from Fidante Partners in relation to the Funds, Fidante Partners is not responsible for the information in this publication, including any statements of opinion.

The information is not intended to be relied upon as a forecast or research and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy, nor is it investment advice. Neither of Fidante Partners nor NovaPort makes any representation or warranty as to the accuracy of the data, forward‐looking statements or other information in this material and shall have any liability for any decisions or actions based on this material. Neither of Fidante Partners nor NovaPort undertakes, and is under any obligation, to update or keep current the information or opinions contained in this material. The information and opinions contained in this material are derived from proprietary and non‐proprietary sources considered by Fidante Partners or NovaPort (as applicable) to be reliable but may not necessarily be all‐inclusive and are not guaranteed to be accurate.