Ageing narratives struggle to find a marginal buyer?

Sinclair Currie, NovaPort Principal and Co-Portfolio Manager

The following article featured on InvestorDaily, 15 June 2021.

In the context of stock markets, Reflexivity is the principle that a higher price for a given stock can improve its fundamentals, and then drive its price higher still. In recent years the small caps benchmark has enjoyed a spectacular run. We believe part of this return has been explained by reflexive, or self-perpetuating trends. Self-reinforcing trends have been supported by 1) a strong narrative, 2) the current market structure and 3) fuelled by a steady supply of marginal buyers. As a result many share prices have spiralled to historic valuation extremes. We highlight that some of the narratives supporting stocks are not ageing well. Their expiration threatens to interrupt the reflexive dynamics underpinning their sky-high valuations. This presents an opportunity for new market leadership to emerge.

HIGHER SHARES PRICES…. DRIVE SHARE PRICES HIGHER

The stock market can enable lucrative opportunities for companies to arbitrage their cost of capital and create value for shareholders. Share prices can work in the same way as a currency (such as our own dollar). For example, a strong Australian dollar allows Aussies to holiday overseas cheaply and buy foreign assets at a favourable exchange rate. In the same way, having a higher share price makes it cheaper for a company to fund growth via acquisition or investment. If the market likes the look of that growth, the share price will likely rise further again, allowing more acquisitions. In this way a higher share price can kick start a reflexive (or self-reinforcing) cycle.

Companies have successfully exploited this dynamic for generations. Reflexivity is most famously explained in detail by George Soros in “the Alchemy of Finance”. A feature of recent markets has been the willingness of investors to focus on revenue growth and ignore profitability. A revenue bias has opened the door for a slew of start-up and speculative ventures to embark on reflexive, share price arbitrage driven growth.

MARKET STRUCTURE ADDS SUPPORT TO MOMENTUM

The current structure of the market has also evolved in a way which adds support to reflexive trends. The growing adoption of passive investing via index funds has created a large, steady flow of dollars which mechanically buy stocks fortunate enough to be included in the benchmark index.

Passive strategies rarely include every stock listed on the ASX. They generally mirror a market index such as the ASX200. This index ‘portfolio’ is selected on the basis of market capitalisation and liquidity. A small company with a rising market capitalisation might be added to an index. Once part of the index, it can then capture passive ‘structural buyers’ which drive the share price higher still. For the growing pool of index funds, the only fundamental that matters is index inclusion and they are structural buyers of these stocks as long as their fund flows remain positive.

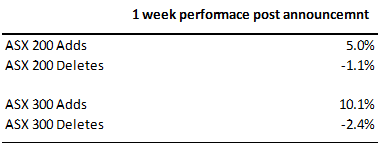

To illustrate the impact of index buying we refer to the below analysis of share price performances of companies initiated into the ASX200 and ASX300 over the days following the announcement of the March 2021 index rebalance. In just one week, the newly ‘initiated’ index members outperformed the ‘deletions’ by 6%. Given the short time frame, we believe buying associated with the index membership change explains most of this performance divergence.

Self-reinforcing dynamics also partially explain why momentum works; because investors believe it works. A quant fund ‘tilted’ to momentum buys stocks which have gone up for the reason that they are expected to continue to go up, which is self-perpetuating. The proliferation of quant based investment strategies using of momentum factors adds a further structural support for reflexive market dynamics.

Funds flowing into passive investment and quant strategies work hand in glove to drive prices higher. Momentum based strategies accelerate the rise of share prices which are rising the fastest. Passive buying then supports this by rebalancing; and investing more dollars into the stocks which have risen the furthest. This market structure has seen the dispersion of valuations between ‘momentum’ and other names explode.

IT ALL COMES DOWN TO MARGINAL BUYERS

The simplistic reason a share price might rise on a given day comes down to the relative abundance of marginal buyers or sellers. A reflexive dynamic is only valuable if the majority believe it works. We think those beliefs are formed by prevailing narratives, the commonly held beliefs investors use to rationalise their holdings.

Over the last decade the underlying factors which have encouraged investors into equities markets have been tepid economic growth and weak wage growth; which have helped contain inflation, kept interest rates low, and driven assets price higher. Over the last 5 years stocks offering growth thematics have outperformed considerably. The narrative underlying their outperformance has been the view that in advanced economies enduring secular stagnation, growth is scarce and thus monetary policy will remain easy.

The pandemic response and change from President Trump to President Biden represent sharp pivots in policy and leadership at the apex of global financial markets. The market quickly decided the pandemic response supported the prevailing narrative however it continues to debate whether the regime change presents a threat to it. We believe it does. However far less attention has been devoted to evidence that in many cases the dynamics driving growth stocks appear to be ageing, badly. The body of evidence appears to be growing.

AGEING NARRATIVES

Underneath the prevailing bias towards growth stocks there are stock specific narratives which explain the willingness of marginal buyers to drive share prices higher. In recent months we have observed the gloss coming off some of these, in both Australian Small Companies as well as globally. Spectacular examples have included Wirecard and Greensill. In those cases it appears that the market did not properly understand the business fundamentals and vastly overestimated their profitability. In Australia we have seen how the market overestimated of the capacity of internet retailers to profitably acquire traffic and convert it into sales. Some of these companies failed to meet expectations despite having made accretive acquisitions.

The growth opportunity in the Software as a service (SaaS) sector is another narrative showing some signs of wear and tear. To assess these companies, Investors typically relied on management representations of: Total Addressable Market (TAM); Customer Acquisition Costs (CaC); Gross Margin (GM); Customer Lifetime Value (LTV) and Research and Development (R&D). In some cases the harsh evidence of accumulated cash burn has begun to challenge the accuracy of these representations. The downside risk is greatest when adjusting to less optimistic assumptions erodes the viability of the growth model.

The danger for investors in these stocks is that the reflexive dynamics which work on the way up, have the opposite effect on the way down. For example, a disruptive software developer might deploy (cheap) capital to fund development of new products which drive growth. If its share price falls because the market finds evidence to suggest it has overestimated the TAM, GM or LTV for these products, the company has less access to the capital it needs to accelerate growth, thus growth will decline.

YET NEW NARRATIVES ATTRACTING MARGINAL BUYERS

To our minds the challenge of small cap investing over the next year is going to be avoiding the painful unwind should reflexive dynamics break down, both at a macro and stock specific level. On a constructive note, the fading of one narrative opens the opportunity for a new sector to attract those marginal buyers.

The transition of market leadership presents and opportunity for investors. We believe investors should consider the impact of governments, technology and consumer preferences. Healthcare, streaming services and undervalued heavy assets all appear interesting areas to search for opportunities. In recent months we have observed unloved companies revealing better than expected earnings updates. Stocks such as Capral Aluminium, Australian Vintage, Sims Limited or MyState Limited have announced better than expected earnings. In many cases these companies have been weakly held by institutional investors, providing ample opportunity for a marginal buyer to have an impact on the share price.

This material has been prepared by NovaPort Capital Pty Limited (ABN 88 140 833 656, AFSL 385 329) (NovaPort). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.